529s Continued

Level 3 - Advanced Concepts

Welcome back! Our previous post on 529s received a lot of questions and follow-ups. We thought it would be helpful to provide some of these questions to everyone in an FAQ format so that we can provide some additional insights to parents, counselors, and other interested parties.

If you missed the previous post, you can read it here:

What advantages are there in using prepaid tuition plans?

When comparing a 529 savings plan and the prepaid tuition plans, some readers asked why a family would consider using the prepaid tuition.

Prepaid tuition plans allow you to buy specific credits or units for a future date, either through a lump sum payment or regular installments. Those credits can then be applied at a future date for tuition and fees at the current “locked in” rates.

Some estimates show that tuition rates at public universities have climbed by 31% over the last decade. If you want to lock in rates and hedge against tuition inflation, this is a great way to do it.

With all of that being said, this may be appropriate if you are in one of the following situations:

You’re confident that your child will attend an eligible university in your state.

You don’t want your education savings tied to the stock market — funds are guaranteed as long as the state’s funding is secure

You don’t want to deal with actually investing the value

What happens if you pay for a prepaid tuition plan and your child does not use the plan?

There are two scenarios where a family runs into an issue with the prepaid tuition plan:

Child applies to and enrolls into public university, but then receives a scholarship where the tuition prepaid tuition plan is no longer applicable.

Child decides to either go out-of-state or to a private college

In the first scenario, you can move the credits that you have purchased to another child in your family. If there are no other children, you can move it to other family member if they qualify as a state resident.

In the second scenario, if a child decides to go out-of-state or to a private college, then what happens next depends on the college your child goes to.

If your child goes to a private school in the state or an out-of-state public university that accepts the prepaid tuition plan, then you will pay the difference between the value of the prepaid tuition plan and the cost of tuition at the other college

If your child goes to college and they do not participate in the prepaid tuition plan, you can receive a refund on the principle that you paid into the plan only.

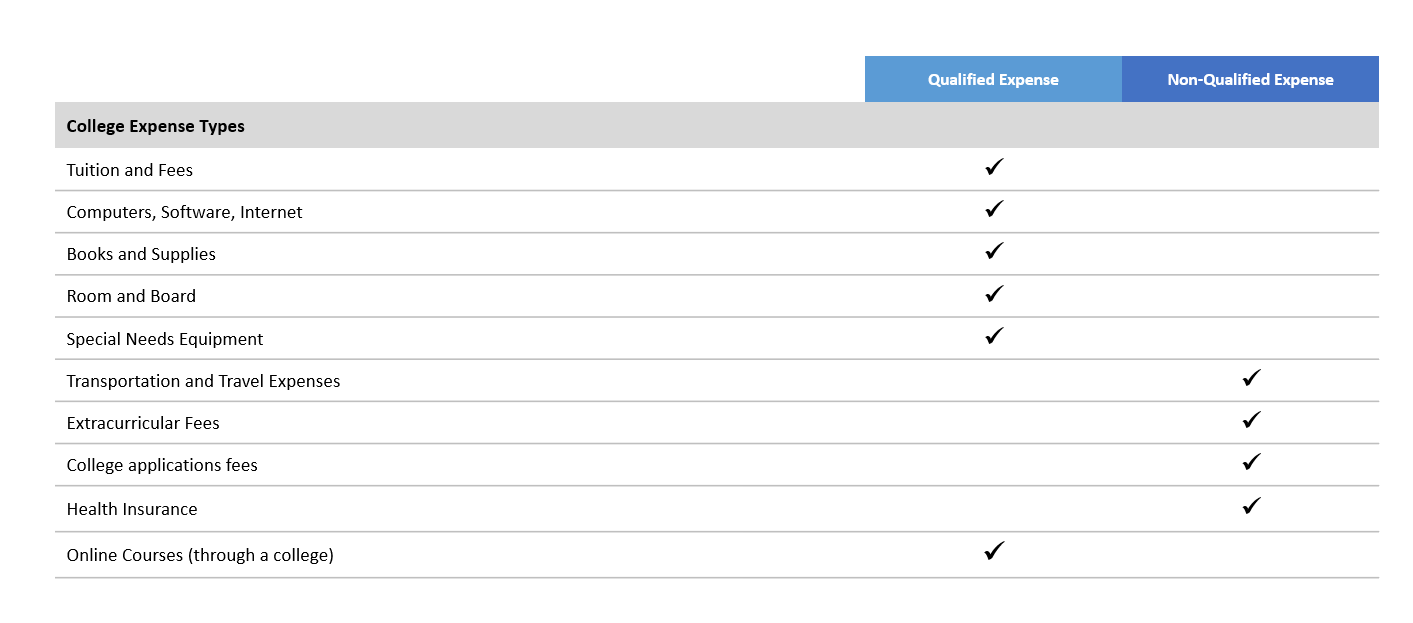

What are non-qualified expenses for 529s?

Although this will vary to some extent between different plans, 529s generally are used to cover certain expenses. One of the questions we receive are the types of expenses that are covered by 529s. Our hope is the below table will assist:

As noted in the above table, this is only for college expenses, and there are nuances with this. For example, room and board are qualified expenses for both on-campus and off-campus housing as long as the student is enrolled at least half-time.

You will want to dive a bit more deeply into these expenses to know how they apply to your specific situation.

And that is a wrap! Have additional questions? We are always open to answering questions, privately and publicly.